Planning for retirement is no easy feat. This is especially true when you’re not born with a silver spoon, or if you’re just starting out. Don’t be discouraged, people gain and maintain their wealth because they are in control of their finances- you can too. Here are a few mistakes many people make to learn from, so you can grow your nest egg and live your dream retirement life.

1. Not starting earlier

You may be young and feel that retirement is decades away, but it’s never too early to start. In fact, it’s important that you start planning now when you’re young, because it’s better to start early. Starting early means that you can take full advantage of the magic of compound interest. On the other hand, the longer you wait, the less time you have for your money to grow, even if you invest more.

Here’s an example assuming that these 2 individuals investments’ grow 4% per annum’:

>> INSERT TABLE <<

Despite saving more than John, Ken’s retirement funds were $26,802 less than John, just because he started 10 years late. That’s the magic of compounding returns.

2. Underestimating the funds needed

You may feel like you don’t need a lot of money to retire in Singapore because the food is affordable, healthcare is subsidised, and your CPF savings is doing a good job helping you with your mortgage. But these will all change when you’re retired and not having an active stream of income. You’ll most likely be living entirely on your savings and CPF, while having to take into account annual inflation. Inflation reduces the value of your money. That means that, as the years go by, you’ll have to pay more for the same goods and services. Global events, such as the pandemic and wars, can increase inflation rate. The core inflation rate of Singapore as of March 2022 is 2.9%, the highest since March 2012. So, do take into account the rate of inflation when you calculate how much you’ll need for your retirement, to avoid under-saving.

Besides, you should also take into account your future commitments along the way before your retirement (e.g. marriage, children, parents, college, car and house payments), so your retirement plan will be on track. This could also better help you manage your wealth and allocate your finances for different commitments at different periods of your life.

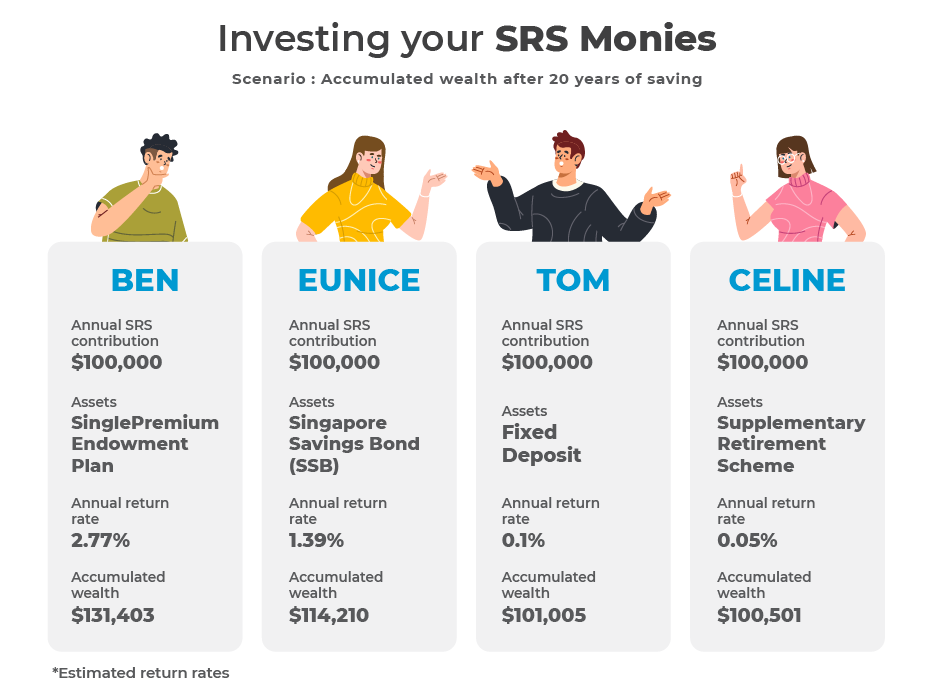

3. Stashing all your money in the bank

While storing your money in the bank feels like the safest way to go, this is actually slowly eating into your retirement funds. As Warren Buffet says, “If you don’t find a way to make money while you sleep, you will work until you die”, storing all your money in the bank is not a feasible way to grow your nest egg, as the interest that your savings account provides is significantly lower than the rate of inflation. This means that your money will slowly lose its worth over time. Instead, you should maximise the potential of your money to earn more money through investments.

Understandably, you might be afraid of high risk investments where you might lose all your money, but that doesn’t mean that you should give up investing completely.

You can first determine your risk appetite, and then make investment decisions based on that. If you have a low risk appetite, you can consider growing your retirement funds through endowment plans or retirement insurance plans that are saving and capital guaranteed, while offering higher interests than fixed deposits. If you are more of a risk taker, you can consider investing in InvestDIY’s Best Investment Funds to earn up to 15.81% p.a.

4. Neglecting your insurance

As you and your loved ones age, illnesses might be more prevalent. It’s important to protect yourself financially, to make sure that sickness doesn’t erase all your efforts for your retirement. Medical insurance in Singapore, which is Asia’s most expensive country to live in, is extremely important, especially if you have dependents (e.g. parents or children) who are financially dependent on you. With the rising cost of medical bills, it’s crucial that you’re prepared to pay for these bills, especially when you’re retired with limited income. As always, it’s better to be safe than sorry.

With the government’s initiative at helping Singaporeans get basic protection against long-term medical care costs, you can also maximise your CareShield Life payouts with supplement plans. Not only will you be able to enjoy additional benefits in the unfortunate event you’re unable to work, you can also use your MediSave for these extra coverages. Choosing the right insurance can help ensure that the people you love the most are protected properly with the best healthcare, while maintaining your progress towards retirement.

With rising inflation rates and medical bills, it’s important to start planning for your retirement and work towards building your nest egg, so that you can enjoy your golden years free from financial worries. Want to know more on how to better plan for your retirement? Speak to our experienced consultants and get answers to your questions.

This is for general information only and does not constitute financial advice. This advertisement has not been reviewed by the Monetary Authority of Singapore.

1 All return figures and other statistics shown above are for illustrative purposes only as past performance are not indicative of future performance or results. Actual returns will vary greatly and depend on various factors and involves risk. It is important to note that the capital value of investments and the income from them may go down as well as up and may become valueless. Some of the statements contained in this website may be considered forward-looking statements which provide current expectations or forecasts of future events. There is no assurance that the conditions described in this website will remain in the future and actual results may differ materially.